Are you curious about how workers’ compensation rates vary across different industries? Understanding these differences is crucial for both employers and employees.

Imagine being able to predict your business expenses more accurately or knowing what to expect in terms of coverage costs if you’re planning to switch jobs. Workers’ comp rates aren’t just numbers on a page; they can significantly affect your bottom line and personal financial planning.

We’ll unravel the mysteries behind these rates, showing you why some industries pay more and others less. Discover how these rates are determined and what you can do to potentially lower them, saving your business money or helping you negotiate better terms in your employment. Dive in to gain insights that could transform the way you approach workers’ compensation in your industry.

What Is Workers’ Compensation?

Workers’ compensation is insurance. It helps workers who get hurt. If a worker is hurt, they get money. This money pays for doctor visits. It also pays for medicine. Workers’ comp protects workers. It keeps them safe from big costs. It helps when things go wrong. Every worker should know about it. Workers’ comp is important. It helps many workers each year.

Many jobs have workers’ comp. It covers many accidents. If someone falls, it helps. If someone gets sick, it helps. Workers’ comp is there for them. It helps families too. Workers’ comp gives peace of mind. It makes work safer. It is a safety net for all. It is there for everyone who works.

Factors Affecting Comp Rates

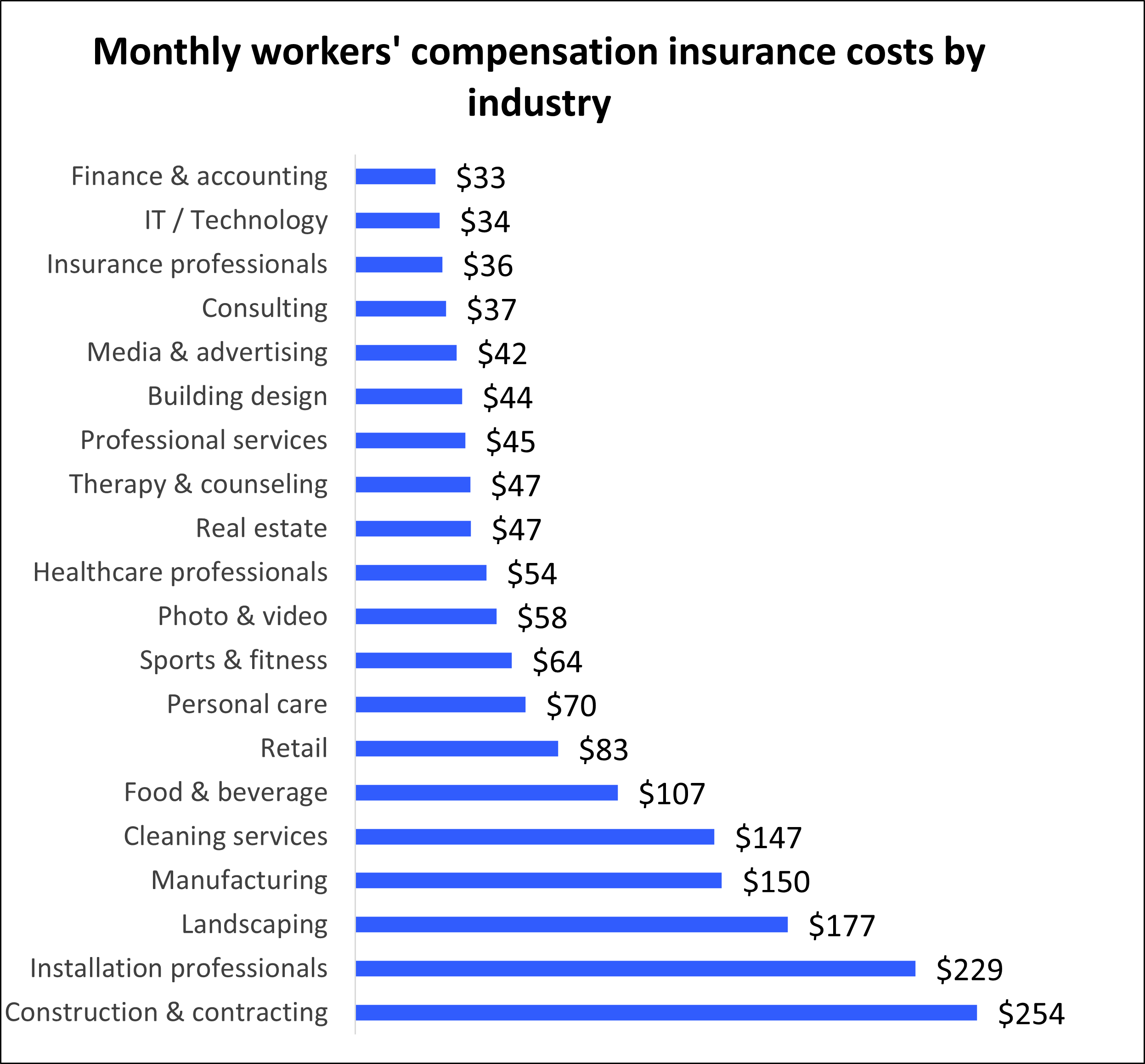

Industries have different risk levels. Construction and mining have high risks. Office jobs have lower risks. Risk affects how much comp rates are. Dangerous jobs need more coverage.

Each state has its own regulations. States set rules for worker safety. Some states have stricter rules. These rules impact comp rates. Rates can change between states.

Safety records matter. Companies with good records pay less. Fewer accidents mean lower rates. Safety programs can help reduce rates. Keeping workers safe saves money.

High-risk Industries

Construction workers often face dangerous environments. Heavy machinery and high places are common. Accidents can happen easily. Workers’ comp rates are high in this industry. Safety gear is crucial to protect workers. Training helps reduce risks. Construction sites must follow strict rules. These rules help keep workers safe.

Manufacturing involves operating machines. Sharp tools and fast-moving parts are present. Injuries are common due to machine mishaps. Workers must pay attention to safety. Protective clothing is vital. Rates for workers’ comp are high here too. Employers should ensure proper training. This helps decrease accidents.

Healthcare workers are exposed to diseases and injuries. Handling patients can be risky. Lifting and moving patients cause strain. Needles and sharp tools are used daily. Workers’ comp rates are significant in this field. Safety procedures are important. These keep healthcare workers safe. Proper training is essential for safety.

Low-risk Industries

Information Technology has low workers’ comp rates. Most work is done at desks. Computer programmers and software developers face minimal physical risk. Office environments are usually safe. Technical issues are the biggest challenge. Injuries are rare. Ergonomic chairs help reduce strain. Healthy practices can prevent issues.

Finance industry is considered low-risk. Bankers and accountants work mostly indoors. Physical demands are minimal. Office settings are safe. Stress and mental fatigue can be concerns. Good work-life balance helps. Injuries are uncommon. Proper posture can reduce discomfort. Regular breaks are beneficial.

Professional services often have low-risk environments. Consultants and lawyers work in safe places. Physical risk is minimal. Mental tasks are more common. Office safety is a priority. Stress management is important. Injuries are rare. Ergonomic equipment is helpful. Healthy habits are encouraged.

How Rates Are Calculated

The Experience Modification Rate (EMR)helps set workers’ comp rates. It is based on past claims. A lower EMR means fewer claims. This usually leads to lower rates. Companies with better safety recordsget lower EMR scores. Safety pays off!

Class codes group jobs by risk. Every job has a code. This code shows how risky the job is. Riskier jobs have higher rates. For example, office jobs are less risky than construction jobs. So, office jobs have lower rates.

Premium discounts are given to encourage safety. Companies with good safety records can get these discounts. This makes their insurance costs lower. It is a reward for being safe. Discounts help companies save money.

State-by-state Variations

Workers’ comp rates differ in each state. Texas has lower rates. California is more costly. Rates depend on state laws. Industries affect these rates too.

Construction work often has high rates. Office jobs usually have lower rates. Agriculture rates vary greatly. Healthcare can be expensive. Each state sets its own rules.

Insurance companies follow these rules. They calculate costs based on risks. Safety measures can reduce rates. Training helps to lower risks. Employers must know their state laws.

Understanding rates helps in planning budgets. Businesses must compare state rates. Choosing a state with lower rates can save money. Small businesses need to watch these costs closely.

Impact On Small Businesses

Small businesses face high workers’ comp costs. These costs can hurt profits. To save money, many choose safety programs. These programs prevent accidents. Fewer accidents mean lower rates. Training workers is key. Safe workers are happy workers. Happy workers work better.

Another way is to review claims regularly. Checking claims helps avoid mistakes. Mistakes can cost money. Set clear rules for reporting accidents. Fast reports mean fast help. Fast help can save money. It’s simple yet important.

Picking the right insurance policyis crucial. Small businesses need the best fit. Some choose group plans. Group plans can be cheaper. They cover many workers at once. Others go for individual plans. These fit specific needs. Always compare options. Get the best deal for your business.

Consulting with an insurance agentcan help. Agents know the market well. They offer advice based on business size. Their guidance can save time and money. Make sure to check their credentials. Trust only the best advice for your team.

Future Trends In Comp Rates

Technology is changing how people work. Machines and robots can do some jobs now. Automation helps work get done faster. It can make some jobs safer. But, it can also take away jobs. Workers’ comp rates might change because of this. Industries using a lot of tech might see lower rates. They have fewer accidents. But, jobs needing people might have higher rates.

Laws help keep workers safe. New laws can change comp rates. If laws make workplaces safer, rates might go down. But stricter laws can also mean higher costs for businesses. They might need to pay more for safety gear. This can affect how much they pay for workers’ comp.

The economy affects job markets. When the economy is strong, more people work. Compensation rates might rise if there are more claims. If the economy is weak, fewer jobs exist. This can lower rates. Different industries feel these changes differently.

Frequently Asked Questions

What Affects Workers’ Comp Rates By Industry?

Workers’ comp rates vary due to industry risk levels. High-risk industries like construction have higher rates. Factors such as workplace safety protocols, past claims, and location also impact rates. It’s essential to maintain a safe work environment to manage costs effectively.

How Are Workers’ Comp Rates Calculated?

Workers’ comp rates are calculated based on industry classification, payroll, and claims history. Each industry has a specific rate per $100 of payroll. Safer industries have lower rates, while high-risk industries face higher premiums. Regularly reviewing these factors can help businesses manage their workers’ comp expenses.

Which Industries Have The Highest Workers’ Comp Rates?

Industries with the highest workers’ comp rates include construction, manufacturing, and agriculture. These sectors involve higher physical risks, leading to increased claims. Ensuring safety measures and compliance can help mitigate these costs. Regular safety audits and employee training are effective strategies to reduce workplace accidents.

Why Do Construction Workers Face High Comp Rates?

Construction workers face high comp rates due to the industry’s inherent risks. Frequent injuries and accidents raise premium costs. Implementing stringent safety protocols and regular training can help lower these rates. Employers should focus on maintaining a safe work environment to minimize claims and reduce expenses.

Conclusion

Understanding workers’ comp rates is crucial for every industry. Rates vary widely. Factors include job risk, state laws, and claims history. Employers must stay informed. Knowledge helps manage costs effectively. Prioritize safety in the workplace. Fewer accidents mean lower premiums.

It’s a win-win. Workers feel secure. Businesses save money. Always review your policy. Ensure it matches your needs. Consult professionals for advice. They offer valuable insights. Remember, informed decisions lead to better outcomes. Protect your team and your business. Stay proactive and vigilant.

Knowledge is power in workers’ comp management.

Read More:

- Commercial Property Insurance Calculator: Maximize Savings Today

- Cheap Whole Life Insurance for Youth: Secure Future Today

- Cost of Universal Life Premiums: Your Guide to Affordability

- Convertible Term Life Policy Benefits: Unlock Financial Security

- Best Car Insurance Rates 2025: Unlock Savings Now!

- Professional Liability Insurance Cost: Essential Budget Tips

- Affordable Motorcycle Insurance USA: Save More, Ride More

- Choosing the Right Family Deductible: A Smart Guide