Are you trying to make the best decision for your financial future but feeling lost in the sea of insurance options? You’re not alone.

Choosing between term and whole life insurance can be overwhelming, yet it’s one of the most crucial financial choices you’ll ever make. Imagine the peace of mind knowing you’ve secured your family’s future, no matter what happens. We’re going to break down the differences between term and whole life insurance in a way that’s simple and easy to understand.

You’ll discover which option aligns with your personal goals and financial situation. By the end, you’ll feel empowered, armed with the knowledge to make the right choice for you and your loved ones. Curious to find out which policy fits your lifestyle best? Let’s dive in!

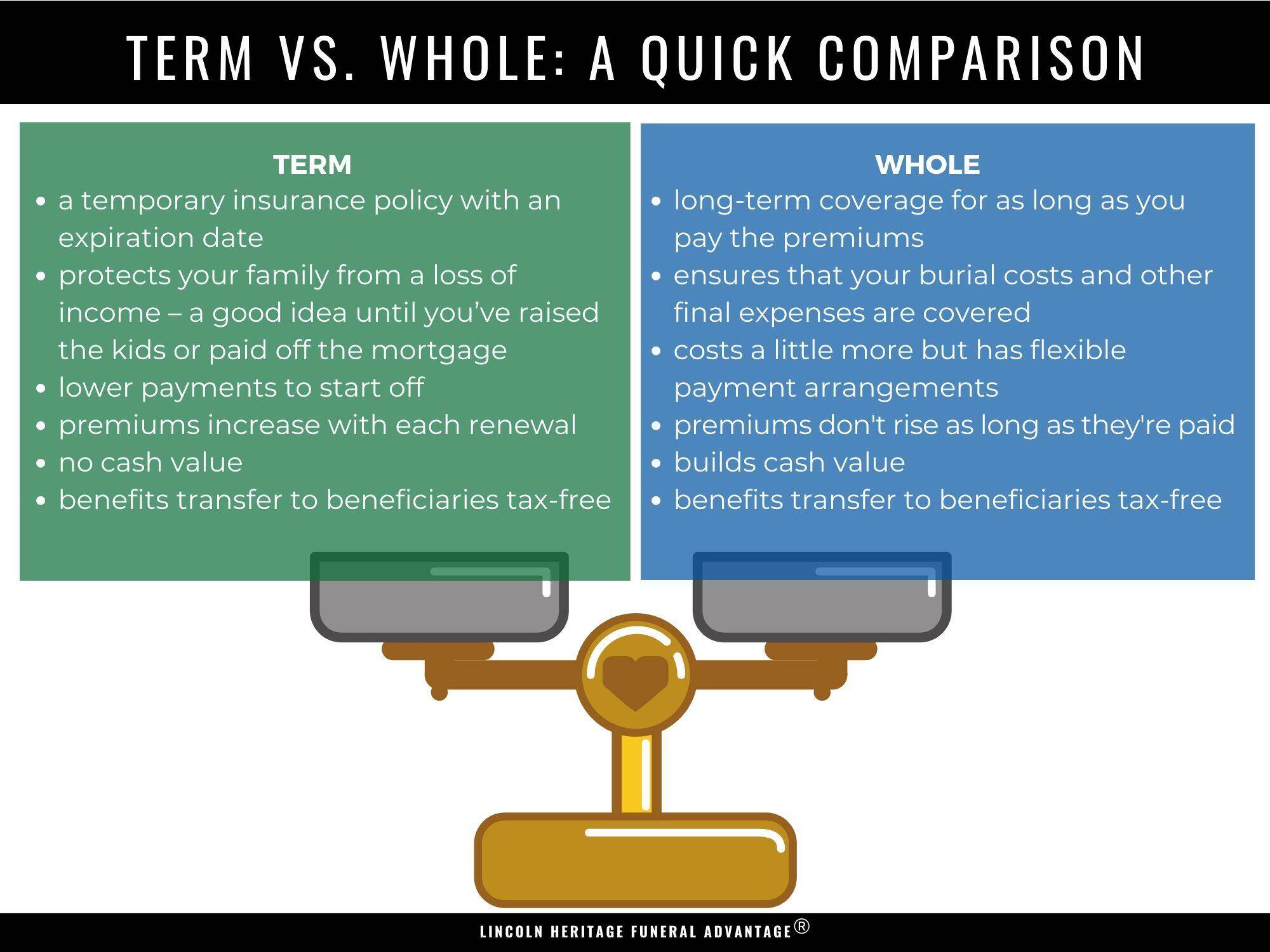

Term Life Insurance Basics

Term life insurance lasts for a set number of years. It can be 10, 20, or 30 years. After that, the coverage ends. You can choose how long you need the protection. This is good for people who want coverage for a specific time.

Premiums are usually lower than whole life insurance. This makes it more affordable for young families. You pay the same amount every month or year. It stays the same for the whole term. This helps in budgeting your expenses.

Term life insurance is simple. There are fewer options to change the policy. You can renew it after the term ends. It may cost more to renew. If you want more choices, look for other options. This policy is straightforward for short-term needs.

Whole Life Insurance Fundamentals

Whole life insurance offers lifetime coverage. This means the policy lasts as long as you live. Your loved ones get money after you pass away. No need to worry about renewing the policy. It’s a one-time decision for a lifetime.

Whole life insurance builds a cash valueover time. This means part of your payment grows. You can use this money later. Borrow it or withdraw it. It’s like a savings plan inside your policy.

The premium for whole life insurance stays the same. You pay a fixed amount every time. No surprises or sudden increases. This makes it easier to plan your budget.

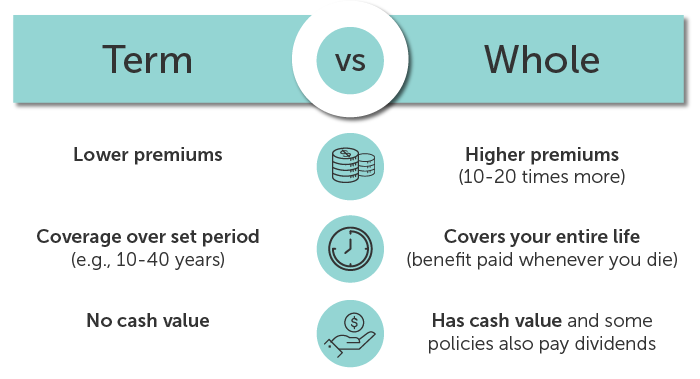

Cost Comparison

Term life insurance usually has lower initial premiums. It’s cheaper at the start. Whole life insurance costs more from the beginning. You pay extra for lifelong coverage. Many choose term for cheaper early payments. But prices go up later.

Whole life insurance might be better long-term. Premiums stay the same. It can be easier to budget. Term insurance is affordable at first. It gets expensive over time. Costs rise as you age. Consider future costs before choosing.

Whole life insurance offers cash value savings. You build value over time. You can borrow from it later. Term insurance doesn’t include savings. It’s pure coverage only. Some find whole life a smart investment. Others prefer term for its simplicity.

Coverage Needs

Term life insurance is great for short-term needs. Whole life insurance covers long-term needs. Term life is usually cheaper. It lasts for a set time. Whole life lasts a lifetime. It builds cash value over time.

Choose term life for loans or young children. Choose whole life for lifelong security. Think about your goals. Decide what you need most.

Different families have different goals. Some want security for their kids. Some want to leave a legacy. Term life is good for immediate needs. Whole life can help with future goals.

Whole life can be part of a financial plan. It can help with estate planning. Consider your family’s future. Choose what fits your goals best.

If a family member dies, income stops. Term life insurance can replace lost income. It helps the family continue living. Whole life can also replace income. But it costs more.

Think about how much money is needed. Choose insurance that covers that amount. The goal is to keep the family safe and secure.

Investment Opportunities

Explore the differences between term and whole life insurance to find suitable investment opportunities. Term insurance offers coverage for a specific period, often with lower premiums. Whole life insurance provides lifelong coverage with a cash value component, potentially offering long-term financial benefits.

Cash Value Growth

Term life insurancedoes not build cash value. Whole life insurancegrows cash value over time. This value can be accessed or borrowed. The growth rate is usually slow but steady.

Investment Flexibility

Whole life policiesoffer less flexibility. The company decides how your money grows. Term life policiesdo not invest money. You pay for coverage only.

Tax Implications

Cash value in whole life insurancegrows tax-deferred. This means you don’t pay taxes yearly. You pay taxes only when you withdraw money. This can help you save on taxes.

Policy Riders And Options

Explore the flexibility of term and whole life insurance through policy riders and options. Riders enhance coverage by adding benefits tailored to individual needs. Options allow adjustments in coverage as life circumstances change, offering personalized financial security.

Customization Opportunities

Life insurance can be tailored to meet personal needs. Policy riders allow for adding extra features. Some riders offer coverage for disability or critical illness. Others can help with long-term care expenses. Custom options let you change coverage for your situation. This flexibility can be helpful for your family.

Common Add-ons

Many choose popular add-ons for their policies. Accidental death rider is common. It provides extra money if death is from an accident. Waiver of premium is another popular choice. It keeps your policy active if you can’t work due to injury or illness. These add-ons can make your policy stronger.

Impact On Coverage

Adding riders can change your policy. Some increase your premium cost. Others may limit your coverage. It’s important to know how each rider affects your plan. Understanding this impact helps make better choices. Choose riders that match your needs. This ensures your coverage stays effective.

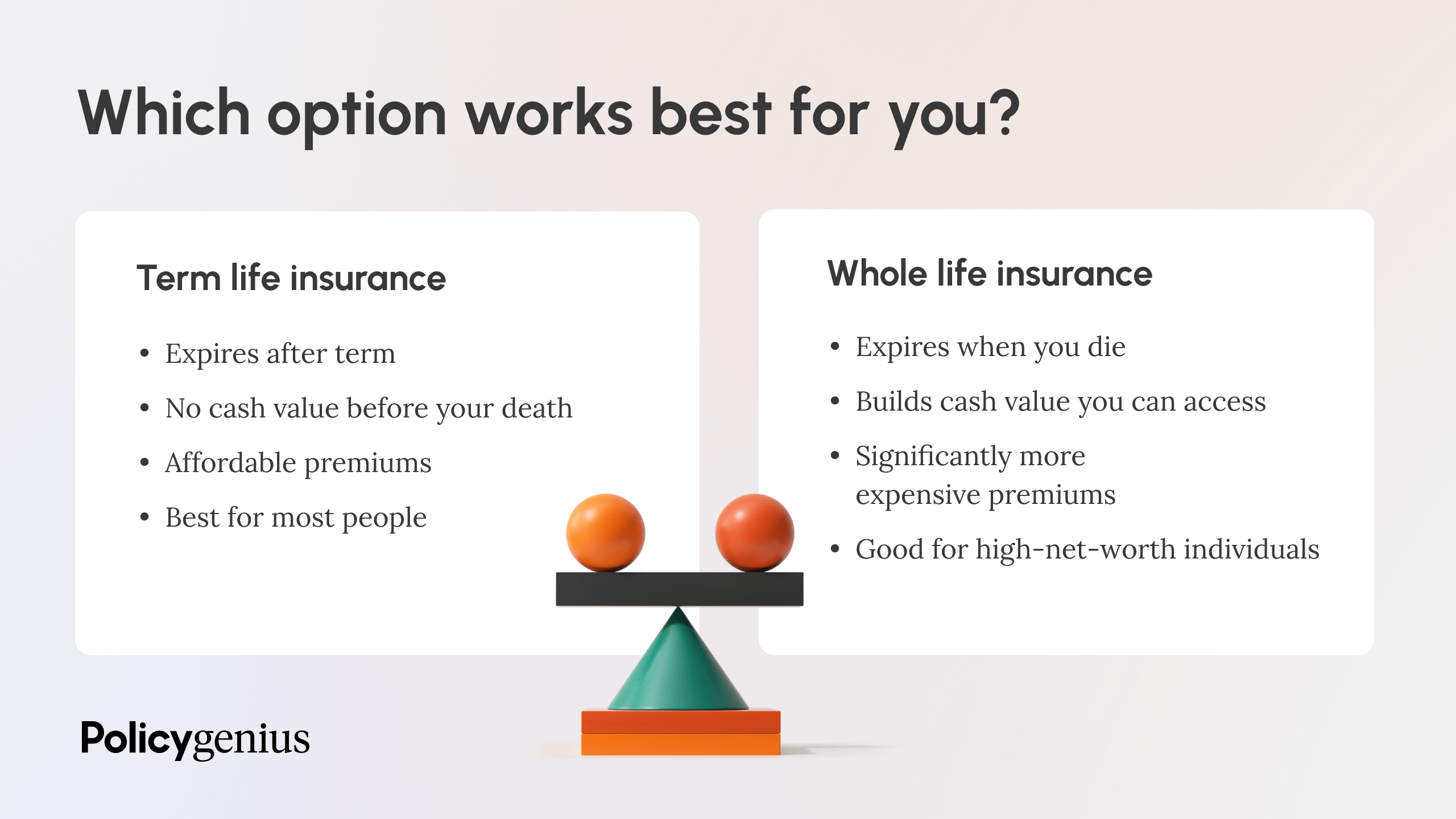

Choosing The Right Fit

Term insurance gives protection for a limited time. Great for short-term needs. Whole life insurance lasts a lifetime. Offers long-term security. Think about your goals. Do you want temporary or permanent coverage? Your choice depends on your life plans.

Term insurance is usually cheaper. Ideal if money is tight. Whole life insurance costs more. But it can build cash value. Consider how much you can spend. Your budget is key in deciding. Think about your current financial health.

Experts can help you make the best choice. They know about insurance. They can tell you about benefits. Ask them about term and whole life options. They can help you find what fits your needs. Advisors can guide you with valuable insights.

:max_bytes(150000):strip_icc()/dotdash-term-life-vs-whole-life-5075430-Final-60fb4e8f7bae43e0a65a3fac2431479c.jpg)

Frequently Asked Questions

What Is The Main Difference Between Term And Whole Life Insurance?

Term life insurance offers coverage for a specific period, usually 10 to 30 years. Whole life insurance provides lifelong coverage and includes a cash value component. Term policies are generally more affordable, while whole life policies can be an investment and savings tool.

Why Choose Term Life Insurance Over Whole Life?

Term life insurance is typically more affordable and straightforward. It’s ideal for covering temporary needs, like paying off a mortgage. It provides financial protection during high-expense periods. Once the term ends, coverage stops unless renewed, often at a higher premium.

How Does Whole Life Insurance Build Cash Value?

Whole life insurance builds cash value through a portion of your premium. This accumulates over time, tax-deferred. You can borrow against or withdraw from it. It’s a financial tool for estate planning, providing lifelong coverage and potential for loans.

Can Term Life Insurance Be Converted To Whole Life?

Yes, many term life policies offer a conversion option. This allows you to switch to whole life insurance without a medical exam. This option is available within a specific timeframe. It’s beneficial if your needs change, offering lifelong coverage and cash value benefits.

Conclusion

Choosing between term and whole life insurance depends on your needs. Term life offers affordable coverage for a set period. It’s straightforward. Whole life provides lifelong protection with a cash value component. It’s more expensive but offers benefits. Both have their advantages.

Consider your budget and long-term goals. Think about your family’s needs. Consult with a financial advisor if unsure. Make an informed decision. Protect your future with the right insurance. Stay secure and confident in your choice.

Read More:

- Commercial Property Insurance Calculator: Maximize Savings Today

- Cheap Whole Life Insurance for Youth: Secure Future Today

- Cost of Universal Life Premiums: Your Guide to Affordability

- Convertible Term Life Policy Benefits: Unlock Financial Security

- Best Car Insurance Rates 2025: Unlock Savings Now!

- Professional Liability Insurance Cost: Essential Budget Tips

- Affordable Motorcycle Insurance USA: Save More, Ride More

- Choosing the Right Family Deductible: A Smart Guide